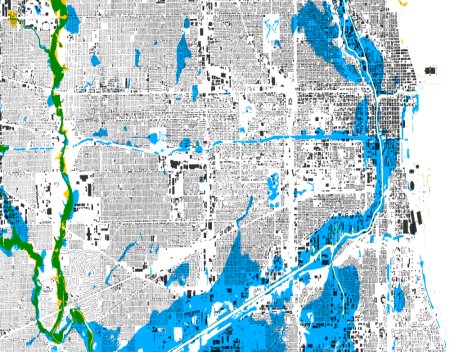

Different Types of Flood Zones

Flood insurance can feel confusing—especially when your premium comes in higher than expected. If you’ve ever wondered “Why is my flood insurance so expensive?” you’re not alone.

As a flood insurance company, we talk to homeowners every day who are surprised by their rates. The truth? Flood insurance pricing is based on very specific risk factors. Once you understand them, the numbers start to make a lot more sense.

Let’s break it down.

1. Your Flood Zone

The biggest factor in your flood insurance cost is your FEMA flood zone designation.

The Federal Emergency Management Agency (FEMA) divides areas into zones based on flood risk:

High-Risk Zones (A, AE, VE) – Higher premiums

Moderate-to-Low Risk Zones (X) – Lower premiums

If your property is located in a high-risk Special Flood Hazard Area (SFHA), insurers expect a greater likelihood of flooding—and price accordingly.

Homes in coastal or river-adjacent areas typically carry higher premiums due to increased storm surge and overflow risk.

Elevation plays a major role in determining your rate.

Insurance companies compare your home’s lowest floor elevation to the Base Flood Elevation (BFE):

If your home sits below BFE, your premium increases.

If your home sits at or above BFE, your rate decreases.

An elevation certificate can sometimes significantly reduce your flood insurance premium.

The more expensive it is to rebuild your home, the more coverage you’ll need.

Flood insurance premiums are partly based on:

Building replacement cost

Square footage

Construction type

Foundation type

Larger homes and custom builds generally cost more to insure.

Your policy choices matter.

Higher coverage limits = higher premium

Lower deductible = higher premium

If you're looking to reduce your flood insurance cost, adjusting your deductible can be a strategic option (though you’ll pay more out-of-pocket in a claim).

The way your home is built affects how water impacts it.

Slab foundations are generally lower risk.

Basements increase risk (and cost).

Enclosed areas below elevated homes can also increase premiums.

Floodwater that reaches finished lower levels dramatically increases potential damage.

Distance matters.

Homes located near:

Oceans

Rivers

Lakes

Bayous

Drainage systems

…are statistically more likely to flood. Even homes not directly on water but in low-lying terrain may see higher rates.

Federal Emergency Management Agency recently introduced Risk Rating 2.0, which modernized how flood risk is calculated under the National Flood Insurance Program (NFIP).

Instead of relying primarily on flood zones, pricing now considers:

Distance to flooding sources

Type of flooding (river, coastal, rainfall)

Property characteristics

Historical loss data

This change has caused premiums to increase for some homeowners and decrease for others.

If a property has a history of flood claims, insurers see it as higher risk. Multiple past losses can significantly increase premiums.

Communities that participate in FEMA’s Community Rating System (CRS) may qualify residents for discounted flood insurance rates.

If your town invests in flood mitigation (better drainage, levees, planning), you may benefit from lower premiums.

While you can’t change your flood zone overnight, you may be able to:

Increase your deductible

Elevate utilities (HVAC, electrical panels)

Add flood vents

Obtain or update an elevation certificate

Review your coverage limits

Shop private flood insurance options

Sometimes the biggest savings come from simply reviewing your policy with a flood insurance specialist.

I have known Tim for many years and he is a man with great integrity, work ethic and one of the nicest persons I know. Over the years Tim has provided insurance counseling and advice to our company, for myself personally, as well as to our clients. Recently Tim, took time to analyze our flood insurance policy and he was able to make some excellent recommendations. Our flood insurance costs are now less and we have much better coverage. I recommend Tim to anyone without hesitation or reservation.

We contacted Mr. Holt for an estimate via email over the weekend prior to a closing on a property, hoping for a response on the following Monday to take with us with confidence in being insured at the settlement table on a Tuesday. He exceeded our expectations not once but in readily responding to the initial request and then to follow-up questions all during the weekend frenzy that occurs before closing. "Impressive and responsive customer service," for sure!

I have no problem giving you an A1 reference for taking care of the flood policies for me and Diane. I appreciate you working with the mortgage company: the surveyor and our previous agent. The result was a 75% reduction in our flood insurance premiums!

We'll help you:

Lower your current flood insurance premiums

Eliminate excessive & unnecessary coverage

Remove the FEMA from the claims handling process